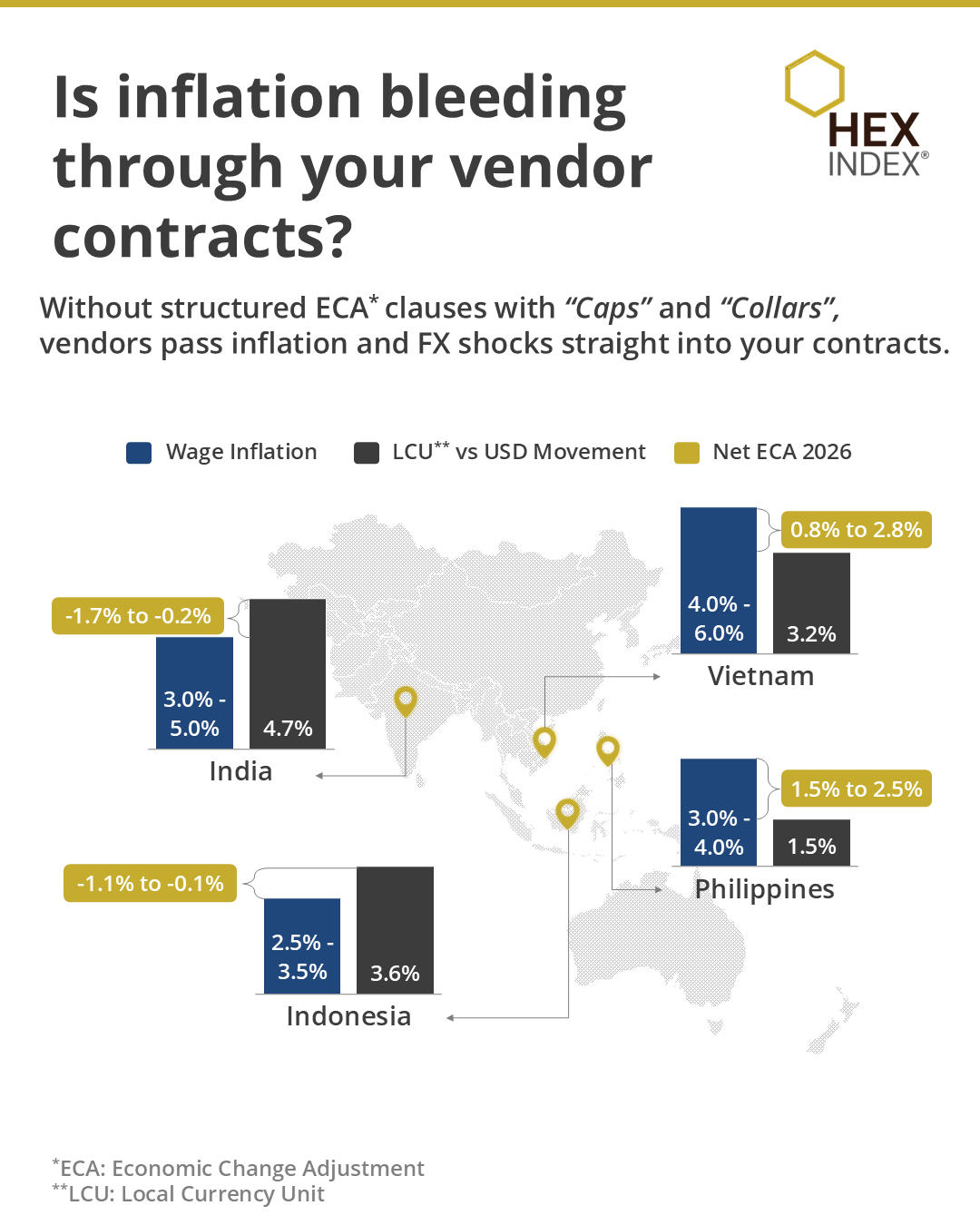

Inflation isn’t just hitting fuel and fares, it’s quietly rewriting your vendor contracts.

If you’re in Travel, Transportation, or Hospitality, those “small” clauses are now cost leak pipelines. FX swings + wage inflation = margin erosion you didn’t approve.

The real question: Are your contracts protecting you or pricing against you?

#HEX Index cuts through the noise with the industry’s only #AI-powered #benchmarking platform, giving you real-time visibility to challenge, renegotiate, and stay ahead of inflation.

Stop absorbing. Start benchmarking.

#Inflation #Procurement #TravelIndustry #CostControl

For years enterprise AI meant one thing.

Use the biggest model available.

That thinking is already outdated.

The next wave of enterprise AI will be built on right-sized models for the right tasks, not GPT-level firepower for everything.

The real shift is not bigger AI.

It is smarter deployment.

Swipe to see what CXOs should actually care about.

#EnterpriseAI #AILeadership #DigitalTransformation #FutureOfWork