Instituting and monitoring the right KPIs helps streamline IT Operations & Budget.

HEX is helping CFOs, CIOs, and CTOs across USA, EU, and APAC to evaluate, recast, and secure the Health of their IT operations.

To know more click here.

Instituting and monitoring the right KPIs helps streamline IT Operations & Budget.

HEX is helping CFOs, CIOs, and CTOs across USA, EU, and APAC to evaluate, recast, and secure the Health of their IT operations.

To know more click here.

Businesses are increasingly adopting SD-WAN to enhance their network infrastructure, streamline their operations and unlock cost savings.

Uncover the adoption triggers and sourcing models of SD-WAN to empower your business to make informed networking choices.

To know more kindly click here.

Automation is not just a buzzword in revenue cycle management—it is a transformative force that is driving healthcare organizations towards a future of enhanced productivity, reduced costs, and improved financial outcomes.

To engage with us click here.

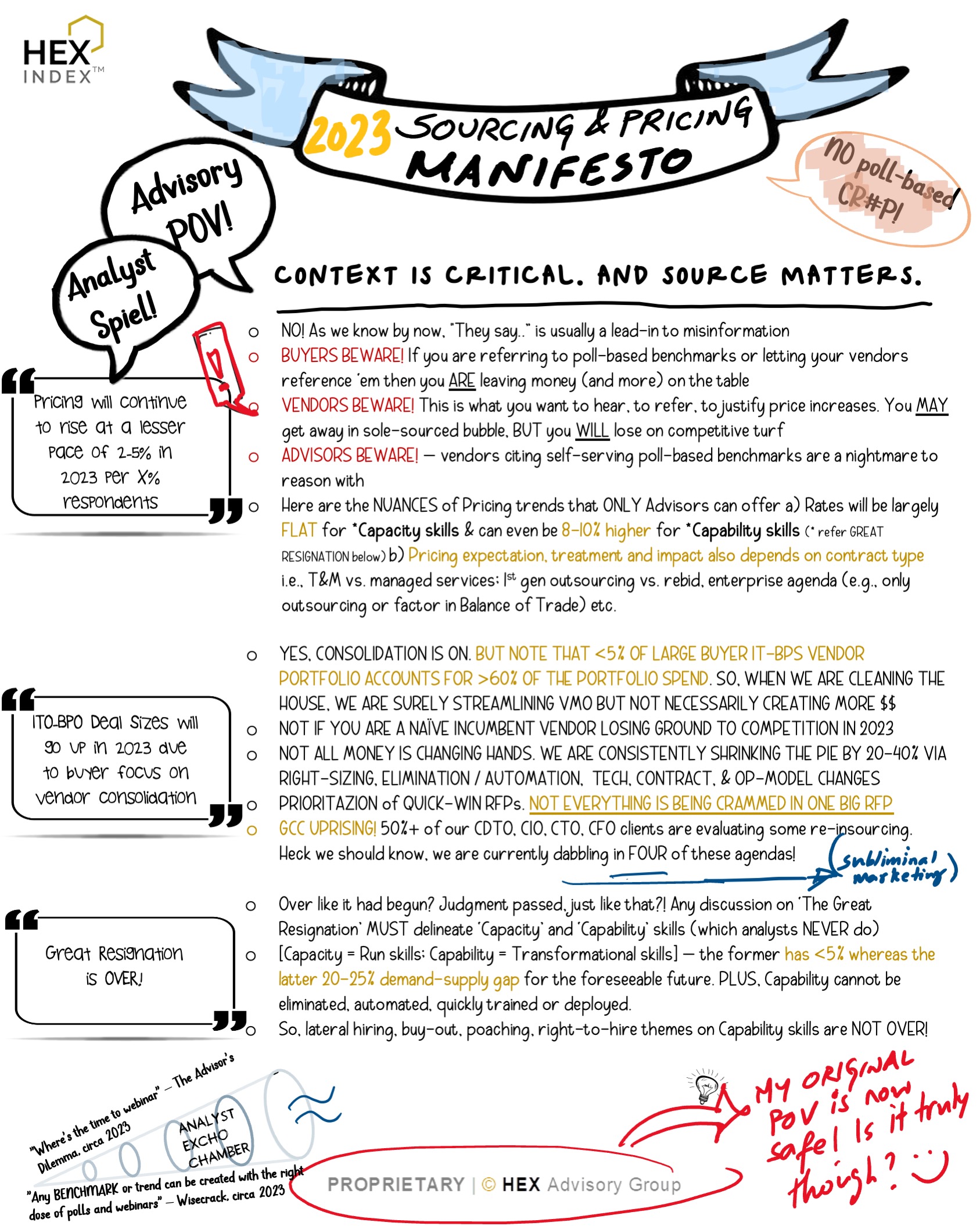

Avoid tacos at 7-Eleven and coffee at Taco Bell. Source matters in everything you consume and that applies to Sourcing and Price Benchmarking trends too.

Don’t ask an advisor what the size of ChatGPT in sourcing deals will be in 2025 and don’t ask a researcher how best to calibrate your multi-million-dollar contracts. You are bound to be misled in either case.

There’s so much broad stroking on IT-BPO Sourcing & Pricing trends going around that I decided not to write a blog post but a MANIFESTO! 🙂

In a BOT model, service provider runs operations in initial stages with an option to transfer back to buyer later. While the operational risk lies with the provider in a BOT model, buyer should staff its employees in all the relevant management layers.

During and post-pandemic, Talent is among the most secular agendas across all firms pan industries. And as firms are scrambling to get the appropriate talent onboard, recruitment process operation is the backbone to execute the talent strategy. As a result, recruitment process outsourcing (RPO) industry has been seeing a sharp growth especially post H2 2021.

A combination of factors are in play that influence enterprises to outsource their recruitment processes.

As a result of the increasing complexity of the health plan environment, coordination of payments to multiple parties and a wide range of government and private health plans remains a challenge. Payment Integrity solutions are reducing the rising healthcare waste and fraud to ensure that claims are paid correctly, free of leakages. Using advanced analytics and data mining, patterns are identified across billions of lines of claims to predict errors in claims, thereby helping firms to reduce waste and focus on value-based care for patients.

We see broadly three types of engagement models in the Payment Integrity space:

What you control is governed by the metrics you measure and report on. But are the right metrics being measured? Traditionally, the functional and back-office metrics have been linked to the respective functional areas and the linkage to enterprise objectives, if at all, may not be evident. The Business Level Agreements (BLAs) framework can help fill this vacuum and ensure that the reported metrics are linked to the business priorities.

Some of the typical BLAs used in F&A processes:

A well thought out set of BLAs is a great mechanism for the support functions (and service providers) to see their impact on the business and the other way round. Enterprises are increasingly embedding these in the contracts to drive risk-sharing and partnership behaviours.

This is an output-based pricing model wherein the fees structure is based on the transactions / Resource Units (RUs) handled. Buyers should consider this model in the following scenarios:

SASE is an emerging technology and organisations must look at it as a journey rather than viewing it as a product. SASE converges the functions of network and security solutions into a unified, global cloud-native service. A SASE solution is meant to provide complete session protection, regardless of whether a user is on or off the corporate network.

The SASE solutions require investment in points of presence and extensive network coverage and on a maturity curve, only an absolute need to put security in the cloud should motivate to consider this as of now; the ecosystem is evolving very rapidly though.

SD-WAN allows for more agile ways of working and improves site availability through simplified and faster failover and relocation of traffic. It helps optimize costs as once implemented, it allows for better aligned demand and supply model to reduce underutilised assets and increase efficiencies as well as utilise a range of cheaper underlying connectivity.

While it offers benefits of technology-agnostic overlay and dynamic routing, without a clear strategy and transformation plan, many of the SD-WAN benefits can be limited or lost such as the ability to consolidate multiple network functions in a single platform.

Virtual captives are increasingly becoming an acceptable solution as they occupy a median position in a spectrum that is occupied by third party outsourcing on one end and captives on the other. For the mid-market enterprises, who end up experiencing a ‘small-fish’ syndrome with large third-party providers and captive remains a pipedream due to lack of capital/appetite, virtual captive offers best of both worlds. It is essentially a hybrid model wherein a local provider will provide all the necessary infrastructure (managed facility, hardware, connectivity etc), talent (sourcing, recruitment & HR), compliance and support services (accounting, compliance, IT operations) while letting the client retain full control of the operations.

Some of the specific advantages this sourcing model offers

Contracts with remit ranging from managed services to supporting Digital Transformation need to clearly delineate the solution and the underlying people and commercial construct. The Capacity and Capability charters are very distinct and painting both with the same brush can lead to a less than an Optimum outcome for both parties.

In this hyperinflationary environment, COLA, once a standard provision, is gaining increasing prominence. And rightly so, as a typical managed services contracts spans 5 years and a robust COLA mechanism/clause that protects the interests of both parties is critical to an equitable contract. It is also in the interest of both Buyer and Seller to include a Benchmarking clause that allows potential commercial ‘reset’ in an uncertain business environment.

Field Service productivity is impacted by SLAs and the underlying support model. The primary driver for productivity is strong emphasis on ticket elimination and “shift-left” of the issues. Productivity can be increased by reducing field service engineers’ intervention. In order to achieve this, service providers can consider strengthening the L1/L1.5 Support with tenured resources to maximize resolution at that level. Furthermore, providers can also consider leveraging following mechanisms to enhance efficiency:

Typically, first gen outsourcing deals / legacy environments have calls and emails as predominant contact channel and proportion of calls and emails could potentially exceed 80-90% of the contacts. However, as service providers rationalize the workflow and implement chat bot and other tools, proportion of calls and emails gets reduced in favour of other channels e.g., chat and web with lower cost to serve. In an end state, service providers may have 60-75% of contact volume by web and chat and remaining 25%-40% by phone calls and emails.

Our advice to enterprises and service providers is to leverage/ contextualize the benchmarks depending upon scope of services and not to have pre-emptive bias for or against any industry. Simply speaking, if scope is a horizontal such as a multi-tower infrastructure deal with its own baselines and environment maturity, then that should drive the benchmark reference set agnostic of industry. However, if we are talking about industry specific scope e.g., payer platform or trading platform support, we’ll need to consider industry specific benchmarks.

Productivity gains and automation impact over the deal term is driven by environmental maturity.. To assess the potential productivity gains, a detailed analysis of number and nature of issues in the current environment is required. We would typically expect overall productivity gains as well as speed of realizing productivity gains to be higher in a legacy (1st time outsourcing) environment v/s 2nd/ 3rd Generation outsourcing deals.

The heated demand is leading to a drive for talent thereby heating up the salaries in onshore and offshore geographies – thereby increasing the cost to serve for Consulting service providers by as much as 10%-20% on a fully-loaded op-cost per FTE basis depending on the underlying technology type and resource seniority. However, enterprises remain cautious and price sensitive on consulting spend and >80% of consulting engagements have some form or fashion of line-of-sight into tangible outcomes / impact.

Currently, the preferred pricing models for S&C are fixed fee based for clearly ring-fenced scope, outcomes, timelines, and with contractual flexibility to pause and/or terminate. Enterprises are also open to risk-gain share mechanisms BUT should be tread with utmost clarity and thought on scope due-diligence, underlying assumptions, dependencies, and outcome versus risk thresholds, else can be detrimental to an already diminishing margin turf for service providers.

Since the cost to serve for S&C is expected to remain elevated in the near to medium term, this segment of business is expected to see margin pressure. A negative margin scenario is only to be expected if providers do not push for a well-defined scope or outcomes, do not size/solution the effort and staffing accurately, or undercut strategically or competitively for downstream execution-led gains. Opportunistically leveraging the perceived ‘premium and niche skills’ market can offer consulting providers with some margin-cushion at a deal-level.

There is an increased enterprise propensity in the market for committed outsourcing outcomes and the same is manifesting itself in increased instances of outcome-based pricing contracts. However, what construes as “outcome” can vary across contracts. Some points to note:

Therefore, the definition of “outcome” may vary, but the model is expected to sustain and gain momentum across contract types.

In managed services contracts, we continue to draft up and get equitable agreement for a 3.0%-3.5% global COLA i.e., applicable to the managed services delivery model incl. the underlying global delivery location portfolio agreed by both parties. The expectation is that the above 3.0-3.5% should be explicitly stated as part of the fee assumptions but needs to be pre-baked into the Y1-Y5 ACV’s i.e., no fee changes during the initial contract term. This incentivizes / encourages the provider to offset COLA against automation-led benefits in the out years, staffing mix and on-offshore mix changes during the contract term etc.

Besides the managed services component, there is typically the project rate card i.e., T&M component in the pricing exhibits. Typically, COLA is applied starting Y3 of the deal & can have higher exposure than managed services COLA i.e., in the 3-5% range depending on skill sets. COLA is subject to the benchmarking clause i.e., if either party wishes to invoke the benchmarking clause to sense-check any significant rate/market changes if the contracted COLA is unacceptable by either party when the need arises

All providers are concerned about the wage inflation, which while real for experienced/lateral hires, needs to be contextualized in the scope of a typical IT-BPS managed services delivery solution. Fact is that the entry-level salaries have remained consistent for the last many years and the same is true even now. Plus, all providers are pushing their entry-level pool to Tier2/3/4 locations and colleges to keep this entry-level cost base consistent, and this is where most providers expect to build 70-80% of their incremental seat capacity esp. with the remote model – most providers have alluded to this in recent quarterly earnings strategies as a margin retention measure. In addition, in a typical delivery AO/IO/BPO pyramid, 75%-80% of the resources are in these bottom two rungs wherein the compensation is being held steady. So, the talent war and the heated 20%-40% wage hikes for experienced hires only applies to 20%-25% of the wage pyramid i.e., 4%-10% net wage increase on a blended wage pyramid. However, wage / compensation is ~50% of a fully loaded offshore rate card (other components being real-estate, telecom/technology, consumables, SG&A, op-margins), therefore, the net offshore rate card impact of blended wage increase is halved to 2%-5%. Now, offshore is typically 80%-90% of the offshore-onshore managed services delivery. Therefore, the net service delivery impact of COLA in a global managed services contract is 2.5%-4.5% and with this rationale we manage to close the agreement at 3.0-3.5% global COLA on equitable and transparent footing.

The mega deals market (>$100M TCV) is shrinking. In general, enterprises are reconsidering large scale transformation investments, breaking down larger programs and staggering them over budget cycles based on priority or predictable RoI. Exceptions may be seen in the Telecom, Transportation, Utilities, Mining, and Energy verticals spurred by the infrastructure spending bill.

Small to mid-sized deals market ($5M – $15M ACV) will continue to see momentum driven by bite-sized initiatives, cost and operations focused mandates, and mid-cap enterprises coming out of the woodwork to sustain their business in a tightening liquidity market. Nearly 60% of new deal value is expected in this segment.

Providers will need to reevaluate their sales strategy – do they invest resources in chasing the few large deals involving long spin cycles or get better at closing smaller deals with shorter spin cycles.

One still sees so many enterprises locked in long term contracts, punitive termination penalties, proprietary technologies, and inflexible financials. Such relationships are the ones where there is seldom any innovation. The provider sees no additional gains to be made from a client stuck in one’s chair whereas the client sees no reason to invest more resources in a lopsided arrangement – and the relationship plummets.

But in an industry so interconnected and stakeholders so transient, the word gets out. Such troubled accounts become competitive targets and the provider starts losing ground. That’s the thing – a contract can have lock in, word of mouth doesn’t.

This may be a bit of memory jog as this is not about the automation BOT that has been the top of mind recall in recent times but rather the good old, Build-Operate-Transfer (BOT) that is making a quiet but definitive comeback to the boardroom discussions. During the pandemic and post ‘The Great Resignation’, firms have and are continuing to de-risk their alternate service delivery models. As part of this, enterprises are increasingly assessing and executing BOT transactions. The drivers for them to do this are multifold e.g., deleveraging third-party outsourced portfolio, managing sensitivities around product development, building digital talent inhouse etc. While the classic BOT remains intact, its close variant, Virtual Captive, is increasingly gaining traction as this model offers a good balance between ‘Control’ and ‘Risk’. The supply side is becoming increasingly mature and arming their portfolios with innovative and agile ‘as-a-Service’ solutions.

Next time, when you are looking beyond Managed Services but do not just have the appetite for own captive, definitely worth adding this to the list of options. Lets you ‘test-drive’ offshore on a ‘Pay-as-you-grow’ model.

Know more about our GCC Lifecycle Advisory Services

Yes, the global growth sentiment is bearish—painful inflation, stocks nosediving, supply chain bottlenecks, war, and whatnot. Why take-on additional risks of switching vendors, reopening contracts, and teasing transformation in this climate, correct? Correct! But have you set boundaries for your comfort zone? Because, if you have not then chances are that you are blurring the lines between that of a practical bear and that of a victim.

Nearly 70% of the IT-BPS transactions that our advisors managed recently were sole-sourced or incumbency vendor renewals / rescoping. Fewer than 20% of these sole-sourced transactions rightfully became competitive when solutioning inertia, contractual impasse, or commercial impracticality was met. In the rest, the enterprises buckled. They sought refuge in notional improvements, tactical promises, and basis point benefits in the face of facts and figures.

Any relationship is worth sustaining and that applies to the contractual kind. However, if you do not set boundaries, you will never know when to rightfully step out. And that is just damaging, no matter the climate.

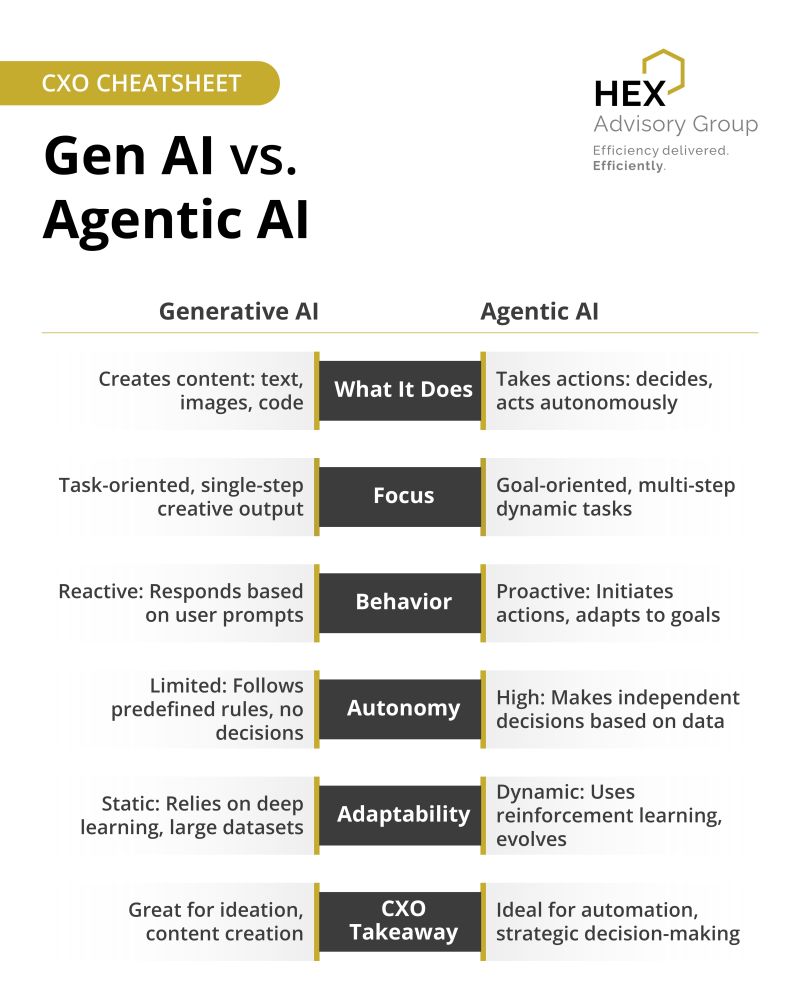

Gen AI is the buzz. Agentic AI is the business. One writes, the other acts. Which one is powering your enterprise?

HEX simplifies this difference through this CXO Cheat sheet.4

Source: LinkedIn

GCCs are heating up and Service Integration providers are switching the tempo.

No-more change the face paint to BOT and perpetuate play. Instead SI C-suite are investing in dedicated GCC leadership, specialized M&As, account-based GCC farming, and augmentative solutions.

Source: LinkedIn

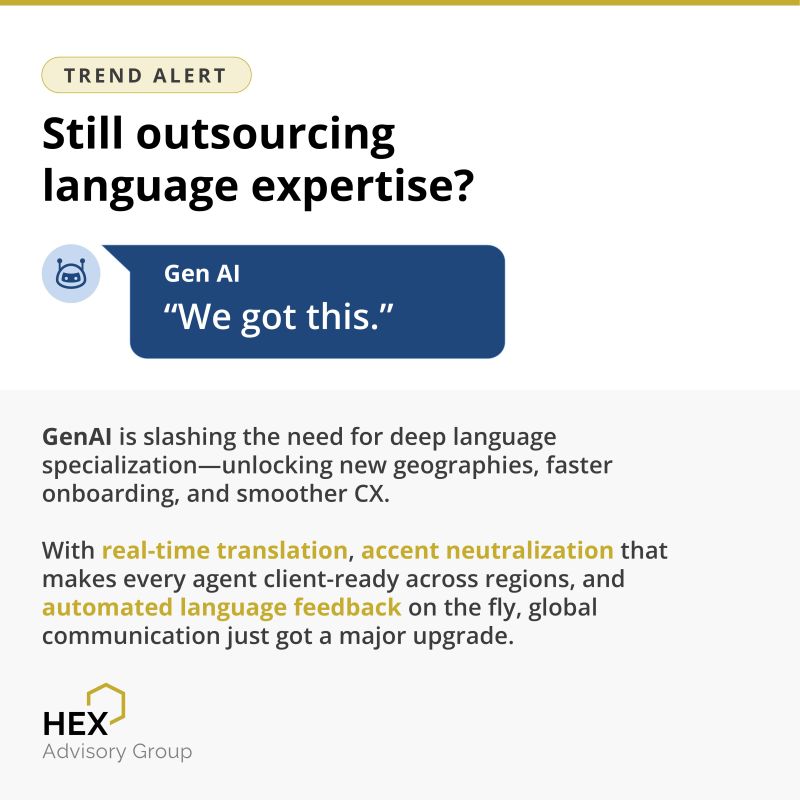

If your scale plan includes 10 new languages and 100 new hires—start over.

There’s a smarter way to do global that too, at scale.

Source: LinkedIn

Is your “independent” advisor a pay-to-play conduit? – siphoning money from hopeful vendors while working on your enterprise dime?

It’s necessary to check for hidden strings when you choose an advisor.

Source: LinkedIn

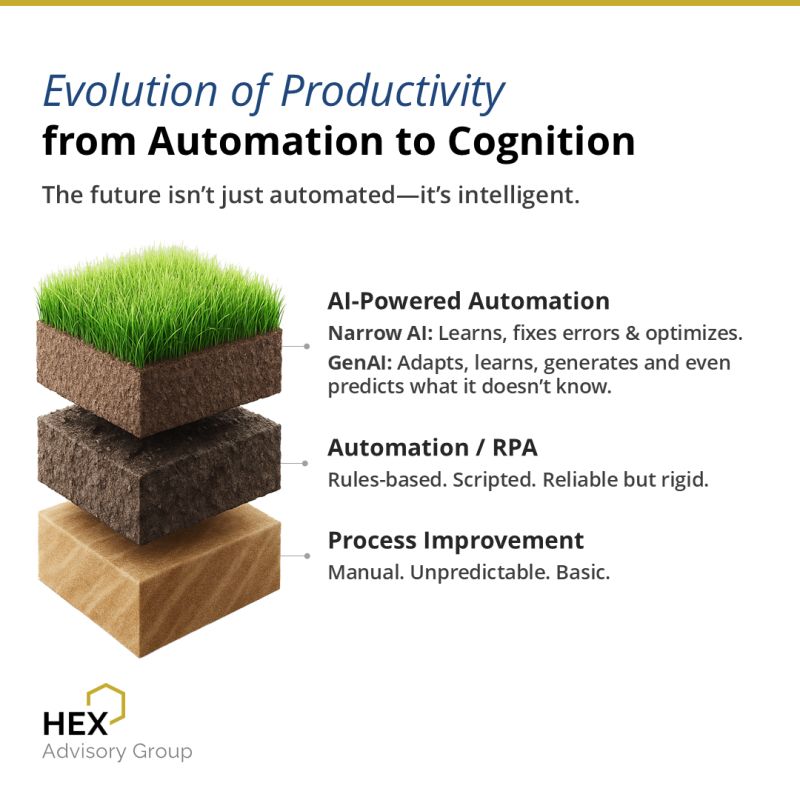

Cognitive automation isn’t the future, It’s the now (thanks to AI)

If your workflows still wait for instructions, they’re already obsolete.

Source: LinkedIn

Sole-sourced deals don’t have to bleed value.

Vendors may price with impunity, but with the right benchmarks and negotiation expertise, you can secure competitive terms, faster turnaround, and significant savings.

Here’s how HEX helped one of the world’s largest hospitality chains achieve market-aligned pricing, equitable terms, and expedited results.

Presenting Part 3 of our series — “Executive Cheat Sheet on T&Cs” — your no-fluff guide to Contracting 101. We break down dense terms and conditions into what they actually mean, why they matter, and how they impact your IT and BPO deals.

This week’s focus: Step-In Rights

Recent trends are redrawing the battle lines in Mid Market Deals.

Bridge the gap with insights that anticipate the shift. Stay ahead or risk falling behind.

This breakdown of GCC providers helps you assess who truly delivers across key dimensions like setup, strategy, and operations.

Are you evaluating your GCC provider with the right lens? Let’s discuss.

Let’s talk: https://hexadvisory.com/contact/#mail

Still running on hold music and manual tickets?

It’s time to replace phone queues with bots, AI, and self-heal.

Want to modernize your service desk?

Let’s talk: https://hexadvisory.com/contact/#mail